Adyen's Free Fall - Part3

Projected EBITDA and Net income for 2H2023 and 2024 and some rumblings on SMBs and Ebay

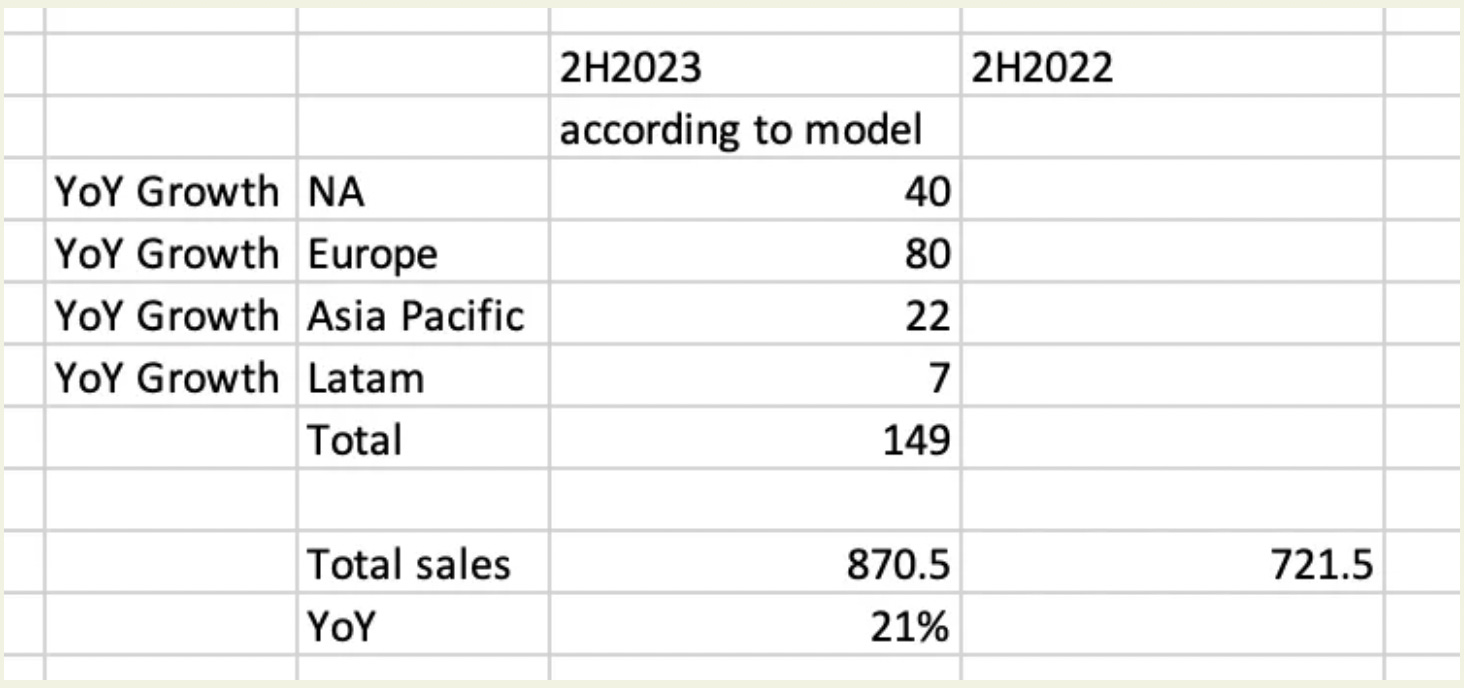

Recap: In the last part of Part 2 of Adyen's Free Fall I published my projected top line based on a YoY growth model per geographical zone as described.

But what about the expense side of it and the bottom line? The current narrative is that Adyen is accelerating hiring and thus bottom line will not raise. My model says otherwise after crunching the numbers!

The article constitutes my personal views and is for entertainment purposes only. This is not an investment advice. The projections and estimates provided here should be considered as purely speculative. Do your own model and projections. Please refer to the disclaimer at the end of this article for more details.

Expenses and estimated EBITDA

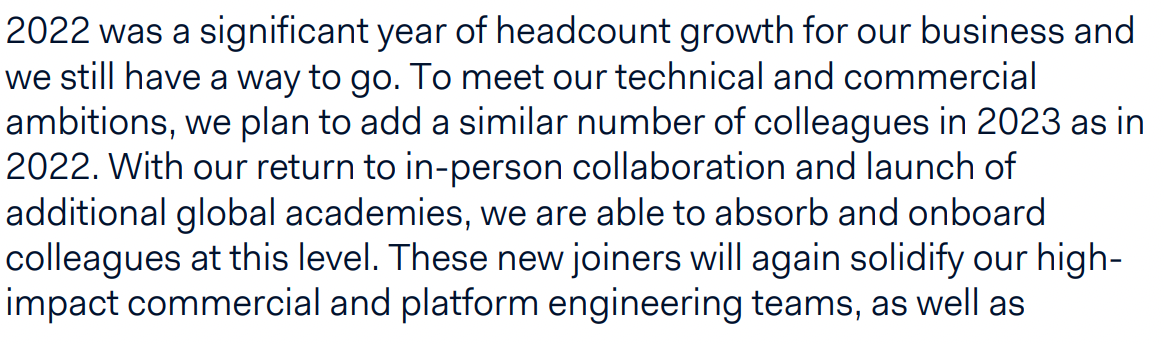

For 2H2023, Adyen is still in accelerated hiring mode. Here is an extract of the latest report:

and the 2H2022

In 2022, Adyen added 1100 employees. Management is planning to add a similar amount in 2023. Since 551 employees were added in the first half of 2023, the same amount should be expected in the second half to get to 1100 employees.

Salaries and wages per employee has been increasing steadily - could be a combination of inflation and hiring for more senior people and in more expensive geography:

1H2022: 52000 euros per employee (6 months cost)

2H2022: 55100 euros per employee

1H2023: 58400 euros per employee

Assuming that we reach 4483 people and a similar rate of growth of 3000 more euros per employee.

Salary and wages for 2H2023 should be: 273m euro.

Shared based compensation will be probably be down significantly such as in 1H2022 due to the price collapse. Let’s put a conservatory 10m euros in that line versus 20m in 1H2023.

For social securities which should increase based on the # of employees I added another 10m sequentially to follow the same growth trend that was seen in the last semester. I kept other expenses more or less stable from last semester as per recent trend.

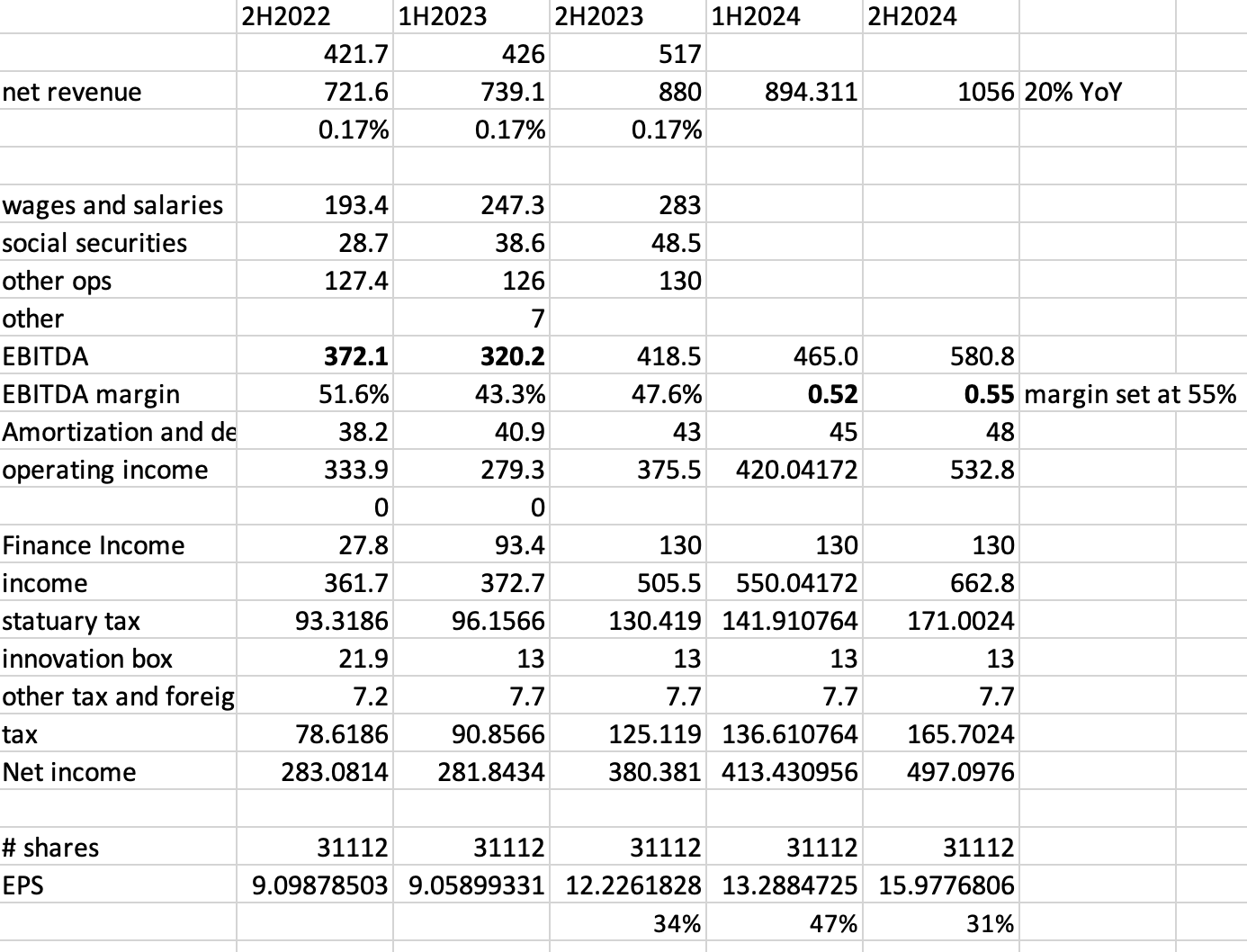

This results in a nice improvement on EBITDA margin to 47.6% and EBITDA of 418.5m.

Net income

Net income should improve significantly due to the EBITDA margin, higher sales and the interest rate increase in the Euro zone. Last semester, the average interest rate in the euro zone was 3%. In the current semester, the interest rate is projected to be relatively flat at 4%. I am assuming a cash yielding balance of 6.4B euros as in last quarter.

As such, the top line will improve significantly to 12.2 euro EPS. This represents a 34% improvement on EPS versus 2H2022.

Projections 2024

In 6 months, the stock for the patient investor will trade based on the expected EPS in 2024. Assuming a conservative growth of 20% of top line (which is below management mid-term guidance of 25-35% range) we could see a significant upward revision of EPS in 2024 with margin going back to 55% in the later part of 2024.

Assuming that 2H2024 improves on margin to 55% from 47.6% in 1 year, the income statement should look at per the following for 2H2024.

According to my model and projection, Adyen will be able to grow EPS by 31% YoY again in 2H2024 to 16 euros EPS for the semester.

Discussion on the accelerated hiring (2022-2023)

Management has been somewhat vague on the reasons for the accelerated hiring growth. Initially, they were mentioning that we were always looking for new quality hire and the 2022 difficult technology slowdown has given them the opportunity to hire more candidates. Based on the recent discussion from management, I believe Adyen decided in 2022 to significantly ramp-up on providing specific solutions for the SMBs via their platform solution. Solutions like easy onboarding of merchants or individual account and account verification. They also need to provide better tracking tools like Stripe is providing for individual merchants on the platform.

Their strategy is to address the SMBs market by enhancing the Adyen for Platform product.

This is explained in the latest Goldman Sachs conference last Tuesday:

So, according to Adyen 1/3 of SMBs gets payment from platform but this will move to 75% eventually. So by focusing all development to serve onboarding and ancillary services to individual merchants via Adyen as Platform, Adyen will be able to serve 75% of the SMBs market.

Adyen is already very strong in supporting individual merchants via platform: Ebay, Wix, Vinted, ETSY, Farfetch and they recently got an entry with Shopify and Amazon in Japan. The last 2 are big wins but I am sure that supporting the last 2 will require significant development and effort. The beauty of serving SMBs via platform is that you dont need to deal with individual SMBs from a sales and marketing point of view, so you can keep a low cost structure.

Ingo has elaborated a bit more on the complete solution they want to provide for the SMBs market as ancillary services:

Discussion on Ebay

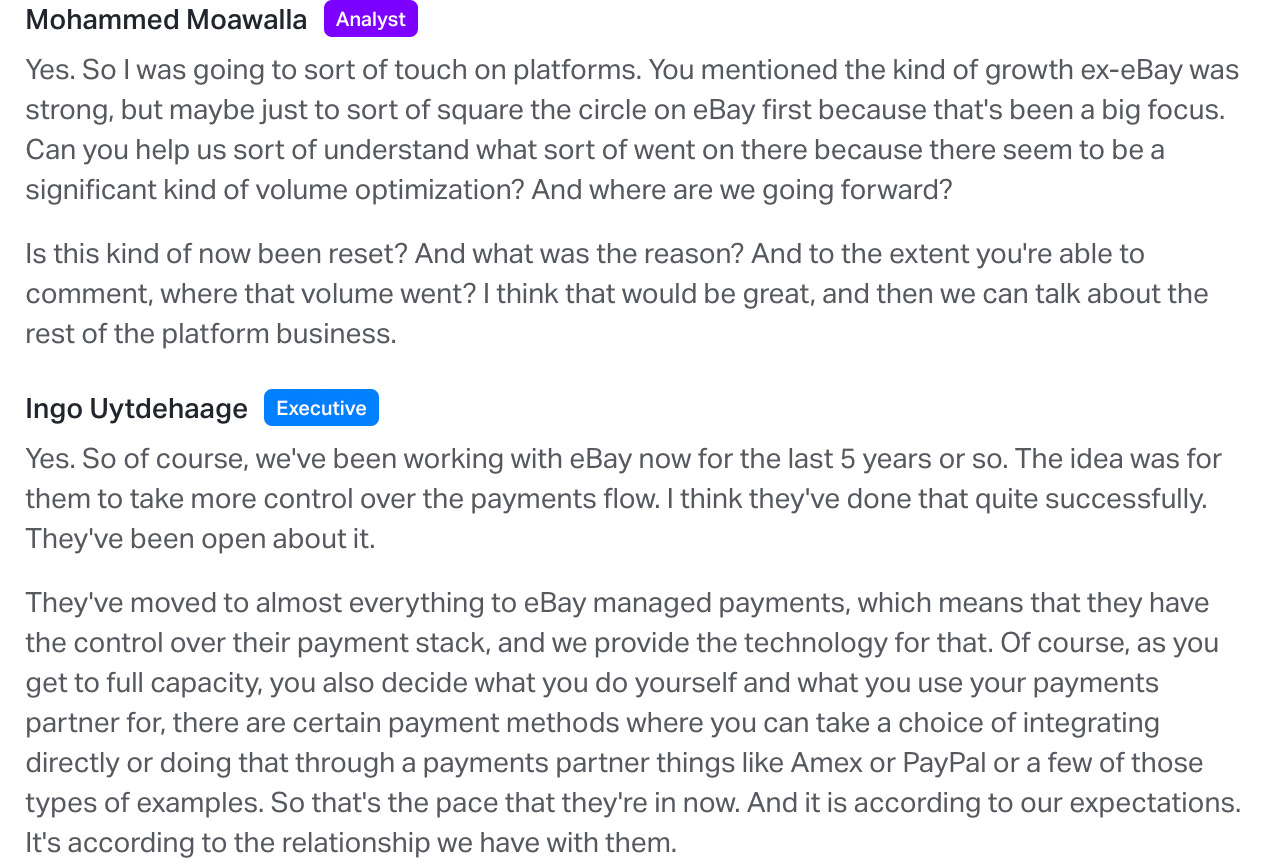

Last week I derived by calculation that about 20% of the Ebay volume move out of Adyen to another platform. Well this was confirmed during the GS call:

So if I read behind the lines, they have decided to process payment themselves for certain types of payment. So instead of all volumes going through Adyen, for certain type of payments, Ebay (using Adyen technology) will process directly those payments. Ingo is indirectly referring to Paypal or Amex.

The following statement then reassures me that the bleeding from Ebay has been stabilized so we shouldn’t get more surprises in 2H2023. They are referring to the warrants that Ebay got from the partnership and the contractual agreement and that the reduction of volume is compliant with the contractual agreement. They also confirmed that on a go-forward basis, internalization is at a stable level.

Historical PE valuations

Adyen is a high priced high growth stock which has always traded at very high multiples. For example, I have derived the historical PE ratio based on the 12 mo forward earnings (actuals not the estimates at the time). As you can observe, Adyen always traded in the 80-120x forward PE range until 1H2022. Then, it traded at around 60x forward earnings until the recent crash.

With the recent 50% crash, Adyen is now trading at 30x forward earnings based on my own estimates for 2H2023, 1H2024 with EPS of 12.2 euros and 13.2 euros respectively. My estimates are shown below.

Historical EBITDA valuations

We can do the same historical valuation using the forward 12mo EBITDA (actuals not estimates at the time). For EV, I simply substracted the cash and cash equivalent from the market cap like koyfin is doing. I know this is misleading since a portion of the cash is restricted due to large merchant payable. However, the cash is income generating so I considered it in the Enterprise Value.

As we can see, Adyen has been trading at 50x EV/forward EBITDA since IPO, with the exception of the year 2020 and 2021 which was above. After recent crash, Adyen has come done to 20x EV/forward EBITDA according to my estimate. This is based on my estimates.

Discussion on Long Term Top Line Growth

I am confident that Adyen will be growing at 20%+ top line over the next 5-10 years for the following reasons:

Industry wide, electronic payment (including Visa and MC, Paypal, debit card) has been growing and is expected to grow at 10% per year over the foreseable future. This is the cash less trend + GDP. So as an industry, legacy players (Fiserv, Wordpay, GlobalPayment) and emerging players (Adyen, Stripe, Checkout, Braintree) combined will be growing at 10% per year. So 10% is a baseline.

Ecommerce is expected to grow even further globally and Adyen is very well positioned in this segment and even more in the unified segment (combination of online and POS). Stripe and Braintree are not strong in the unified segment. A lot of merchants have both a retail presence (e.g LVMH (Sephora), and an online presence. A payment processor that can handle both on a single platform is very important. This is not the case for legacy players.

Some legacy players like WorldPay are weak and much larger than Adyen. WorldPay is made of multiple mergers of companies. There is no unified code base. Any upgrade or development of new services is problematic. So emerging processors like Adyen, Stripe, Braintree, Checkout have been winning merchants and taking share from legacy players. The trend will continue.

Adyen through the Adyen for Platform product is going after the SMBs market and will start competing with Stripe and Braintree in this segment. Refer to the recent win with Shopify (a long time partner of Stripe) and Amazon in Japan.

The company has maintained a target of 25-35% top line growth in the mid term future.

Recent weakness is confined to NA and is partly explicable to the Ebay internal effort to process internally some of the payment types. The current level of internal process is supposed to remain stable according to Adyen’s management. Besides NA, YoY growth is following the same trend as before as shown in the previous post Part 2.

Discussion on Bottom Line Growth

The unit economic of a business like Adyen are very favorable. They have a single unified SW stack all developed internally and with limited usage of 3rd party SW. The more volume you process the more SW development cost is amortized over a larger volume. Management has communicated frequently that EBITDA margin is targeted to be 65% over the long term. Until recently it was hovering over 55%. My projection for 2H2023 is seeing an improvement to 47% from 43% sequentially. As such, the bottom line will improve at a faster rate than the top line. On top of that, as Adyen processes more volume and free cash flow cumulates, cash and cash equivalent will raise steadily over the following years. If volume processed double over the next 4 years (20% CAGR) as I am expecting, cash balance could double.

As such, I think it is likely to say that EPS should grow by 25-35% over the next few years. My current estimate is 34%, 47% and 31% for the next 3 semesters.

Valuation rumblings

A company growing EPS at 25-35% in a industry lite business where almost all cash flow ends up in the bottom line (Adyen spends about 6% of net revenue on capex in average), should normally trade at a very high multiple.

Historically it has been trading at higher than 60x forward earnings. Other SW companies like Cadence, Synospsis are currently trading at 60x earnings. This is not uncommon for high quality SW company. But now Wall Street is panicking. Jefferies just came out with a neutral recommendation on Adyen at 740 euros. The narrative is that Adyen has lost its competitive edge. NA sales will stale. The last time Adyen was trading at 750 euros, it was in 2019, when Adyen was barely known and had earned 5.75 euros EPS in the last 12 months, so still trading at more than 100x trailing earnings.

My own analysis which I have spell out in the 3 articles is that Wall Street is too pessimistic. That growth trend in other geography has not been broken and will continue and that NA growth has slowed because of one time or transitory volume adjustments (Ebay, possibly Uber) and even if NA is worse than I expect, the RoW represents 75% of Adyen’s projected growth.

The reason I am holding and increasing my holding at this price is that once worst case scenario are out of the way - and we may have to wait until early February results are out - the stock will be quickly repriced upwards.

I am not putting at target price. I will let the intelligent readers figure out what it the right price, but for me this is worth significantly more than 750 euros.

Disclaimer: The above article constitutes my or the authors’ personal views and is for entertainment purposes only. It is not to be construed as financial advice in any shape or form. Please do your own research and seek your own advice from a qualified financial advisor. I / The authors may from time to time hold positions in the aforementioned stocks consistent with the views and opinions expressed in this article. The information provided in this article is not making promises, or guarantees regarding the accuracy of information supplied, nor that you guarantee for the completeness of the information here. The information in this article is opinion-based and that these opinions do not reflect the ideas, ideologies, or points of view of any organization the authors may be potentially affiliated with. The authors reserve the right to change the content of this blog or the above article. The performance represented is historical" and that "past performance is not a reliable indicator of future results and investors may not recover the full amount invested.

Thank you - I think your salary estimates are way too low. 59 kEUR ~ in tech role is too small in Amsterdam example as SW you get around 100 kEUR salary

Very detailed and thorough analysis. However, I am wondering if the growth slowdown in NA is primarily related to EBay, why wouldn't the Adyen management call it out as such? thanks